|

Tuesday, February 25 2014

Despite many publicly aired fears to the contrary, it’s safe to say the Brisbane of 2034 will not look vastly different to the 2014 version. Beyond the boundaries of the inner city, where an estimated 50 extra skyscrapers are expected to rise in the next 20 years, the status quo is anticipated to remain among the vast majority of the river city’s suburban landscape. Just seven per cent of the city’s land mass will be impacted by development in the next two decades and 40 per cent of the city will remain devoted to green space. More than 150 urban villages will rise but leafy backyards will remain. City Plan 2014, Brisbane Lord Mayor Graham Quirk said, will create a city Brisbane residents can continue to enjoy and be proud of. Tuesday, February 25 2014

Australian house prices are set to keep growing by around 6% annually in the next 12 to 24 months. The latest NAB quarterly residential housing survey showed that housing market sentiment lifted again in the December Quarter, supported by faster house price growth in all states except South Australia and the Northern Territory. NAB's forecast expects average capital city house price gains of about 6% this year. Queensland is set to lead the country, with Brisbane prices to increase 6.4% this year and 6% in 2015. Perth house prices are expected to grow 6.3%. Monday, February 24 2014

The Reserve Bank of Australia has noted while weak conditions in the labour market had weighed on consumption growth, the increase in housing and equity prices over the past year had raised the possibility that consumption growth could outpace that of income in the period ahead. The board members noted in the February minutes that the effects of low interest rates were clearly evident in the housing market, where prices had increased further and turnover had picked up to be just below average. "These conditions were expected to provide further support to new dwelling activity over the period ahead, and leading indicators of dwelling investment had increased," the minutes noted. The members also observed that the softness in commercial construction meant that there was labour available to support the strong growth of higher-density dwelling construction. Growth of housing credit was gradually picking up, particularly so for investors. The members discussed the staff forecast for the domestic economy, which was a little stronger over the next year or so than at the time of the November Statement on Monetary Policy, in part due to the lower exchange rate. GDP growth was expected to strengthen a little through 2014, though would be likely to be at a below-trend pace. Growth was then expected to pick up to an above-trend pace by mid 2016. But the outlook for the labour market was little changed, as the effect of the softer tone of the recent employment data had been largely offset by the slightly stronger growth outlook. The inflation forecasts had been revised higher, reflecting a combination of the lower exchange rate and the higher-than-expected December quarter CPI outcome, slightly offset by a softer outlook for wages growth. Underlying inflation was expected to be around 3 per cent over the year to mid 2014 and was then expected to decline towards 2.5 per cent. Members recognised that conditions in the labour market tended to lag economic growth, and that the labour market had remained weak following the period of below-trend growth in activity. The minutes noted further signs that the expansionary setting of monetary policy was having the expected effects, with more timely indicators having been more positive for consumption, dwelling investment, business conditions and exports. "Although inflation in the December quarter had been higher than expected, there were several possible explanations. "The Board noted that it was likely the inflation reading contained some noise as well as some signal about inflationary pressures, but also presented something of a puzzle in interpreting the mix of activity and price data. "Also, the further depreciation of the exchange rate since the December meeting was expected to add to inflation for a time, although the outlook for slightly slower wage growth was expected to help keep domestic cost pressures contained over the medium term. "At recent meetings, the Board had judged that, given the substantial degree of monetary policy stimulus already in place, it was prudent to keep policy unchanged while assessing the continuing impact of that stimulus." Paul Bloxham, chief economist at HSBC suggests the bottom line was today's minutes reinforced the RBA's shift to a more neutral policy bias and their greater comfort with the current level of the AUD. "The outlook for the labour market and the degree of persistence of recent strength in inflation will be key factors determining the timing of future rate hikes. "We see the RBA's easing phase as done and also see it as likely that the RBA may need to lift the cash rate before the end of the year," Paul Bloxham said. Tuesday, February 18 2014

MacQuarie bank has predicted two further rate cuts this year. There view is not shared by all including the RBA which is expecting a pick up in GDP to 2.75%. ONly time will tell Friday, February 14 2014

If you are considering upgrading your property you may be looking at your existing home and feeling it could make a good investment property. Whether it is the right move for you will depend on a number of factors. Many people assume they can simply redraw or set up a new loan on their old home (which will become an investment property) and claim that debt as a tax deduction. This is not correct. Contact us for an initial discussion.

What are the secrects you need to know before you start investing?

All the best Greg Carroll Friday, February 14 2014

Not all properties are treated equally by lenders. There are some properties that lenders like, some which they will have restrictions around, and some which they just won't touch at all. What does this mean for you. It means you may not be able to fund a particluar property purchase of they you may have to tip in additional cash to get the deal across the line Below are some the the property types where lenders may have restrictions or may not fund at all.

Units less than 50m2 Number of units in one complex Lenders may also choose to restrict their exposure to certain apartment blocks. If they have already financed a number of purchases in a particular complex they may not support any further transactions. Inner city units and hi-rises Serviced apartments/Student accomodation Lenders may need to see additional detail to determine the level of acceptable lending. In particular they will want to see the current letting agreement and if there are any restrictions associated with having the property released from the letting pool. Commercial property Company title Heritage listed Warehouse conversions Multiple units on one title Rural property Aged care security and retirement villages Vacant land Thursday, February 13 2014

ONE of the country’s biggest banks expects house prices to rise as much as 20 per cent before the end of next year, with lifts predicted to begin soon in parts of Queensland. ANZ chief economist Warren Hogan told the Committee of Economic Development of Australia that the “housing market is at the early stages of a solid cyclical upswing” fed by low interest rates and market shortfalls. “We expect a 15-20 per cent lift in home prices between 2013 and 2015,” he said with long-awaited rises already underway in Sydney and Melbourne. “I am sure Brisbane, Sunshine Coast and Gold Coast will lift in terms of house prices in the next little while,” he said in the Sunshine State yesterday. Mr Hogan said investors and “new participants” in the market — such Chinese and other overseas buyers who typically did not need to borrow in Australia - were pushing increases. “They’re quite active and their judgment on what is fair value for property is very different from others in the market,” he said. “I think that’s something to keep an eye on.” But experts agreed Australia was not in a house price bubble yet. Commonwealth Bank head Ian Narev said: “We never say never — but we don’t think we are seeing even the early signs of a bubble at the moment.’’ Queensland Treasurer Tim Nicholls said there was no evidence of a housing bubble in the state. “In Queensland we’re seeing steady but moderate growth in house prices, so we’re not overly concerned about a bubble here,” he said. “We think that Queensland growth rate is about right. We’d like to see some more growth coming through in terms of the number of houses and approvals coming through, but in terms of prices, we’re not seeing a bubble coming through here.” Mr Hogan agreed it was not a bubble “but it could be”. “If you whack the big four banks together, the system is only growing at five per cent, even though we’re writing new mortgages at 18 per cent ... Overall credit growth is still quite tepid so you wouldn’t say that that’s a bubble.” Wednesday, February 12 2014

Asbestos materials of various types were commonly used in Australian property construction between 1940 and 1990. Asbestos materials were embedded in wall cladding, roofs, gutters, drain pipes, vinyl flooring, electrical wiring thermal insulation, boilers, exhaust pipes, switchboards, thermal insulation and inside fire doors. The new National Work Health and Safety Act of 2011 requires owners of buildings constructed before 2003 to conduct an asbestos survey. Where asbestos materials are identified, this triggers the mandatory requirement for an asbestos register and asbestos management plan (AMP). Some property owners appear to be unaware of this new obligation. An asbestos register is necessary to track of asbestos materials remaining (or removed) in investment properties. Asbestos may also be located in inaccessible areas and unfortunately discovered during re-development with sometimes disastrous and costly results. Asbestos materials if disturbed can cross contaminate internal areas of the buildings, requiring evacuation, loss of rent and potential occupant litigation. Asbestos removal is a legally notifiable project, which can result in extremely costly asbestos removal projects. Careful investigation during due diligence can forewarn investors, revealing the true cost of asbestos removal. Armed with detailed information and cost options, investors can then more accurately evaluate if they wish to proceed with the purchase or avoid the risk. Wednesday, February 12 2014

Australia’s economic growth is expected to pick up pace this year thanks to a lower exchange rate and stronger activity in the housing and retail sectors, according to the latest forecasts from the Reserve Bank of Australia. Investment in the mining and resources sector is forecast to peak some time this year and a pick up in the non-mining sectors of the economy is needed to maintain economic growth. “Until recently, survey measure of current business conditions have been below average, consistent with subdued non-mining investment,” the RBA said in its quarterly statement on monetary policy. “A number of indicators, however suggest a gradual increase in growth over time.” “The depreciation of the exchange rate should provide some additional impetus to activity in the traded sectors of the economy,” the RBA said. The bank said that business conditions improved in the latter part of 2013. “Retail sales and the Bank’s liaison point to a pick up in household consumption growth in the December quarter and measures of consumer sentiment remain a little above average levels,” the RBA said on Friday. Wednesday, February 12 2014

While Sydney and Melbourne’s property markets may struggle to sustain their phenomenal recent growth rates, Brisbane is being tipped to benefit from its ample room for capital growth and rental yield potential. Brisbane’s property market is showing signs of growth early this year, which is good news for buyers seeking a relatively affordable investment. RP Data’s research director Tim Lawless suggested this week that while the “investment fundamentals” are waning in markets such as Sydney and Melbourne, investors might turn to Brisbane because it’s much earlier in the growth cycle. The stage that a property market is at in the growth cycle is influenced by the level of supply and demand. In Brisbane’s case, increasing demand could certainly see values climb above the current median of $462,000. Throw in the city’s solid rental yields, which are hovering round the 5% mark and notably higher than averages in both Sydney and Melbourne, and there’s plenty of reasons for optimism. Monday, February 10 2014

The housing market is in the early stages of a solid cyclical upswing, buoyed by low interest rates, but it's not a bubble, ANZ Bank chief economist Warren Hogan says in a Committee for Economic Development of Australia report. "Our view is that prices remain largely explained by low interest rates, sharply improved affordability, the release of pent-up sales demand created over recent years and an unprecedented (and increasing) shortage of physical housing stock," Hogan writes. He says the majority of future price gains will be in Sydney, Perth and Melbourne, with investors driving the upturn in the market. Friday, February 07 2014

Leading agent John McGrath has forecasted that the strongest east coast market over the next three years was likely to be south-east Queensland. "The market I am really excited about is south-east Queensland." "Prices in Brisbane and the Gold Coast are still below pre-GFC levels, while Sydney is about 10% above now, so there is a greater likelihood of better capital growth in the sunshine state over the next few years." Currently, the median house price in Brisbane is $470,000 whereas Sydney is $775,000. Brisbane’s median apartment price is $383,000 compared to $557,000 in Sydney. RP Data also provides joint Brisbane-Gold Coast data showing a 4.9% growth in house prices and 2% in apartments. McGrath says a "phenomenal spring season" in Sydney last year, I was expecting another good year for Sydney," but the strongest market over the next three years is likely to be south-east Queensland. "In short, we ain’t seen nothing yet! We’re just at the beginning of the recovery." McGrath suggests of south-east Queensland. Friday, February 07 2014

If you have a capital loss it is carried forward until you make a capital gain. Other losses are treated differently. For example if your business or rental property loss pushes your current year income below zero, you are entitled to carry that loss forward into the next financial year, but first you must reduce it by any exempt income you have received, for example Centrelink family payments. Further, you cannot pick and choose when you offset the loss. It must be used up immediately. This can mean it is wasted. For example if you have a $10,000 carried forward loss but only have $15,000 in taxable income in the following year then the loss from the previous year must be used to reduce your taxable income down to $5,000. The loss is wasted because you would not have had to pay tax on the $15,000 anyway. Tuesday, February 04 2014

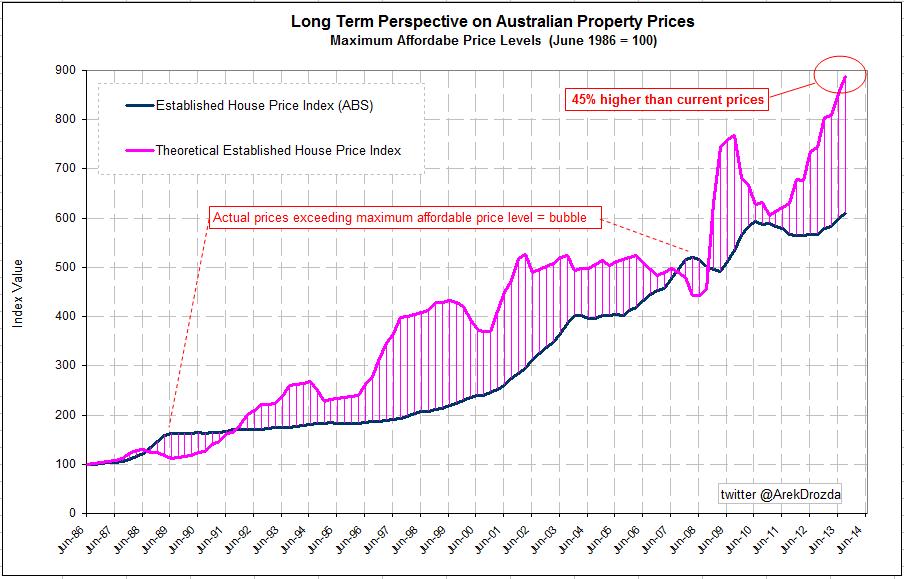

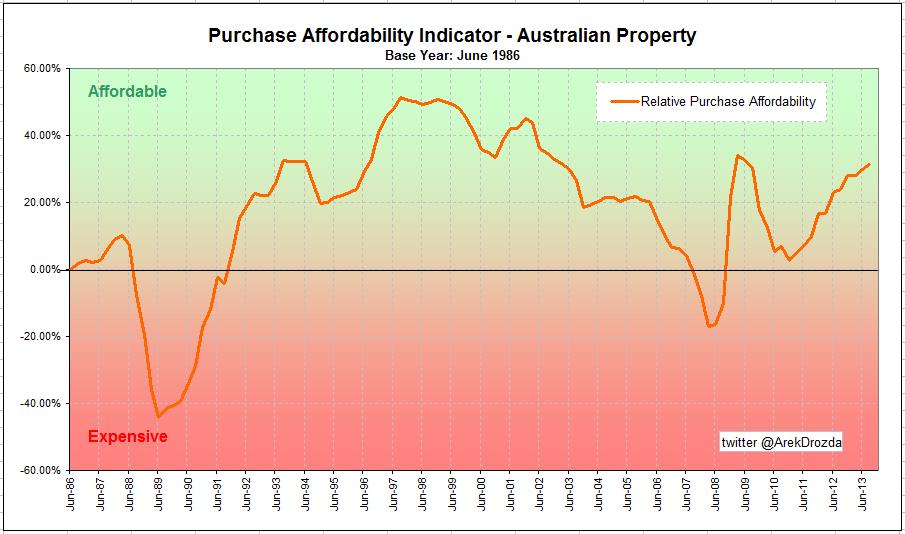

In interesting article I came across last week below. Australian property prices in 2014 and beyond - a peek into the future By Arek Drozda In my previous article, 'Australian property prices explained', I presented a chart that provided very accurate narrative on what has happened in the Australian property market over the last three decades. It is safe to conclude that the same concept which allowed for the description of the past with such accuracy, should also be able to provide a reasonable guidance for the future. Of course, predicting exactly what will happen in 2014 and beyond is a tall order. Life is known to create such a variety of unanticipated scenarios that the reality will almost certainly play out differently to what everybody expects. Therefore, I prefer to think about the future in terms of a range of possible outcomes and likely probabilities of occurrence rather than as a single, definite result. The real benefit of such an approach is knowing how changes in economic conditions can potentially affect the outcome - not in picking the exact end result in advance. Since changes in some economic factors will have more profound effects than others, if you can identify in advance what are they, you can watch out for the tell-tale signs that a particular scenario is playing out – and act accordingly. You only need to be right about the direction property prices are heading to be able to benefit. Please consider what follows with caution - in the “what if” category, rather than a certainty. Based on the income capacity of working Australians, residential property in this country is not overpriced and prices are far from bubble territory. The proof is in relative changes in the cost of buying over the last 27 years, which has been significantly below the relative changes in personal incomes over that time. Below is a slightly different representation of that information to highlight this point.

By rearranging the data we can create a chart that shows how much more property prices could increase at present and still be considered affordable (in relation to current incomes and as benchmarked to 1986).

The above chart indicates that current property prices are potentially undervalued by as much as 45%. Of course, this does not mean that prices will immediately move by this much but the potential for a substantial jump is there. Yet another perspective using the same underlying data reveals that conditions are now starting to resemble those in 2009. Although affordability in 2009 was not as extreme as in late 1990’s, it nevertheless led to a substantial price increase in 2010.

Therefore, as history shows, if interest rates remain mostly unchanged and incomes keep growing, we can anticipate a significant jump in property prices in coming years. The increase could either be a rapid advancement of 10-20%, or even 30%, in the next 12-24 months if the 'good times' perspective prevails or, if pessimism dominates, it could result in an even more substantial jump but in the more distant future. Of course, this scenario can only play out on the proviso that there are no unexpected shocks applied to the system, such as a major international conflict, another economic calamity in the region, another collapse of world financial system, or a major natural disaster – to mention a few obvious cases. In terms of further outlook, if the relationship between costs of buying, incomes, rents and prices hold in the future, and the current rate of income growth continues, then it can be estimated that from now to the end of 2023 property prices could grow by as much as 140% under a historically low interest rate scenario (i.e. 5% per annum), or as little as 20% under a high interest rate scenario (i.e. 10% per annum). Under a more probable scenario of slower growth in incomes and interest rates averaging 7% per annum over the next decade, prices can still be expected to grow by 60% in the next 10 years. A much gloomier future is also possible but the probability of this scenario is rather small at this point in time. That is, a 40% drop in property prices is possible in the next decade but it would take extreme economic conditions for this scenario to play out. In particular, mortgage rates would have to persist at close to 20% per annum for a good part of the decade and income growth would have to drop to 2% per annum to bring prices down by this much. In conclusion, the outlook for property prices in Australia is positive - unless of course the world encounters another economic disaster of a magnitude that is hard to even imagine. Some insist that the next big event is 'just around the corner' so, it would be wise to keep an eye for the tell-tale signs of possible troubles brewing somewhere in the world but there is no obvious reason to panic just yet. Arek Drozda is an independent analyst who has worked in the public and private sectors for over 20 years in business development, data analysis and in building geographic information systems. Tuesday, February 04 2014

The TD Securities – Melbourne Institute Monthly Inflation Gauge has risen 0.1% in January, in a significantly more benign result than the 0.7% rise in December. In the 12 months to January the inflation gauge increased by 2.5%, following a 2.7% rise for the 12 months to December. Seasonal adjustments leading to price rises in education, urban transport fares and utilities were offset by falls in the price of clothing and footwear, holiday travel and accommodation as well as books and stationery. Prices for fuel, fruit and vegetables were relatively flat, according to the inflation measure. Head of Asia-Pacific Research at TD Securities Annette Beacher said that the result is particularly noteworthy given January is traditionally a strong one for the gauge, which has risen on average by 0.4% for the month in the last seven years. The results come ahead of the Reserve Bank of Australia’s first board meeting for the year today, with Beacher predicting that the US Federal Reserve’s tapering schedule and recent emerging market concerns are likely to be significant talking points. |